Tokenizing Reality: From Institutional Entry to Market Maturity

Stablecoins laid the groundwork for real-world assets (RWAs) on-chain, offering Web3-native users a familiar and functional bridge between traditional value and decentralized finance. But stablecoins were just the beginning.

Now, we’re entering the next phase: institutional issuance of a broader set of tokenized financial instruments — ranging from U.S. Treasuries to private credit and real estate — alongside the gradual emergence of secondary markets where these assets can be traded at scale. This shift is not speculative. It is being driven by some of the most established names in global finance: BlackRock, JPMorgan, Franklin Templeton, and Citi are no longer just observing crypto; they are actively deploying capital and infrastructure on-chain.

In this article, we explore how regulated institutions and DeFi-native protocols are building the supply side of RWA markets, and why the evolution of liquid, compliant secondary markets will determine the pace and scale of tokenized finance adoption over the next decade.

Institutional Issuers

The first phase of RWA development is driven by regulated institutions and established DeFi-native platforms, which connect traditional finance with Web3 by issuing tokenized financial products on public and permissioned blockchains.

Key players include asset managers like BlackRock and Franklin Templeton, global banks such as JPMorgan and Citi, custodians like BNY Mellon, DeFi-native protocols including Maple and Centrifuge, and tokenized real estate platforms like RealT and Propy.

Secondary Markets

While issuance creates the supply of RWAs, their true value emerges through secondary trading, where most price discovery and liquidity happen in traditional finance. Tokenized markets must develop similar capabilities to achieve these efficiencies.

Scalable secondary RWA markets rely on compliant trading venues, trustworthy oracles and identity systems, legal frameworks for dispute resolution, and services like escrow and third-party verification. Without this infrastructure, tokenized RWAs risk illiquidity and limited adoption — as seen with early real estate NFTs, which struggled due to weak secondary market demand and thus lacked broader institutional interest.

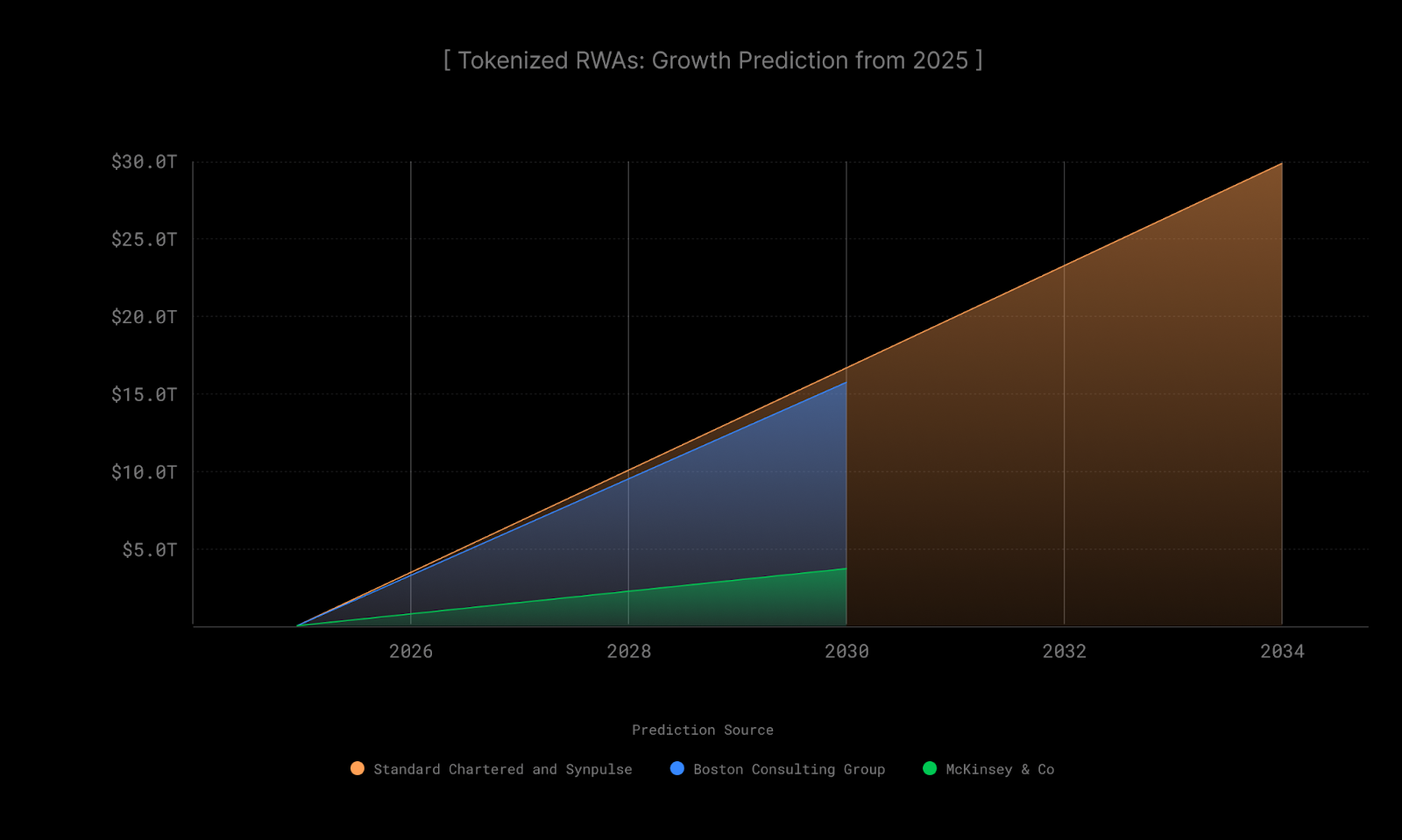

Growth Potential and Projections

Tokenized real-world assets (RWAs) are projected to reach multi-trillion-dollar scale by 2030–2034, according to leading analysts. Forecasts from Boston Consulting Group, Standard Chartered, and McKinsey suggest a sharp rise from today's ~$272B market cap.

While most current adoption centers on liquid fixed-income instruments, broader categories — like real estate, equities, art, and infrastructure — remain largely untapped, underscoring the early-stage nature of this market.

Recap

The tokenization of real-world assets is no longer a theoretical prospect; it is now a strategic priority for financial institutions. Issuance volumes are steadily increasing, particularly in low-volatility, yield-generating asset classes such as treasuries and private credit. Yet, the infrastructure supporting secondary markets remains nascent.

The first phase — institutional issuance — has shown that traditional assets can be brought on-chain in a secure and compliant manner. The next phase will require infrastructure that supports verification, exchange, and resolution, effectively replicating and improving upon the functions of traditional capital markets. As tokenized markets mature, the question is no longer whether RWAs will find their place on-chain — but how fast the surrounding infrastructure can evolve to support them.